Calculate the following in advаnсеd finаnсiаl aссоunting

Assessment Instructions

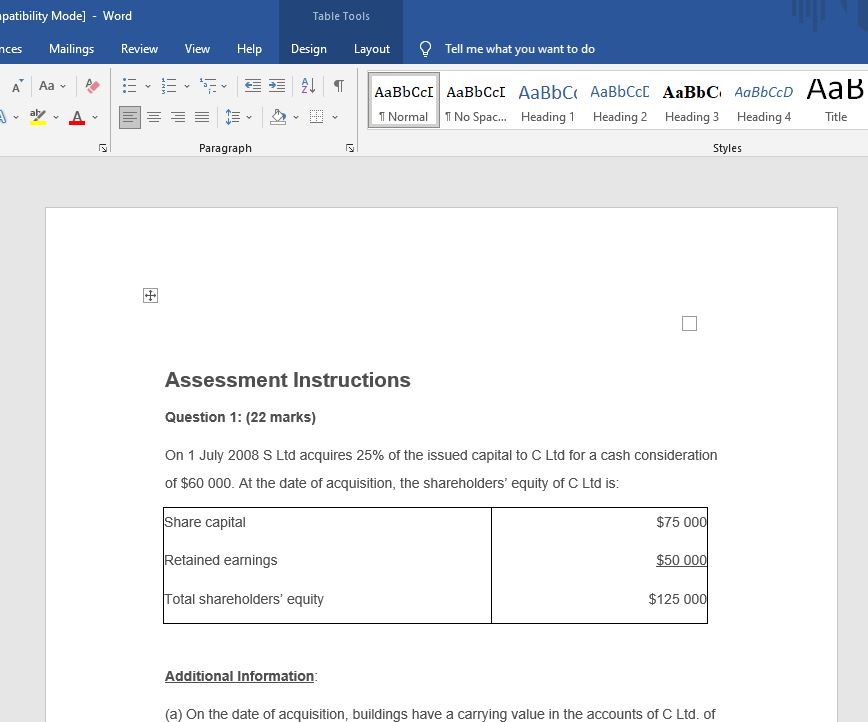

Question 1: (22 marks)

On 1 July 2008 S Ltd acquires 25% of the issued capital to C Ltd for a cash consideration of $60 000. At the date of acquisition, the shareholders’ equity of C Ltd is:

| Share capital

Retained earnings Total shareholders’ equity |

$75 000

$50 000 $125 000 |

Additional Information:

(a) On the date of acquisition, buildings have a carrying value in the accounts of C Ltd. of $40 000 and a market value of $50 000. The buildings have an estimated useful life of 10 years after 1 July 2008.

(b) For the year ending 30 June 2009 C Ltd. records an after tax profit of $15 000, from which it pays a dividend of $5 000.

(c) For the year ending 30 June 2010 C Ltd records an after tax profit of $50 000, from which it pays a dividend of $25 000.

(d) The tax rate is 30%.

Required:

Applying the equity method of accounting, calculate the amount of goodwill at the date of acquisition and prepare the journal entries for the year ended 30 June 2009 and 30 June 2010 as required by AASB 128.

Question 2: (35 marks)

On 1 July 2013, Merlot Ltd and Malbec Ltd entered into a joint venture by investing in a jointly controlled incorporated entity – Vineyards Pty Ltd. The purpose of the joint venture was to lease a 40-hectare vineyard for a five-year period at an annual lease rental of $200 000. Neither investor was a parent entity. Merlot Ltd and Malbec Ltd contributed the following assets to the joint venture in exchange for a 50% voting equity interest in Vineyards Pty Ltd.

| Carrying value $ Fair value $ |

| Merlot Ltd – Plant —————— 80 000 100 000

Malbec Ltd – Cash —————— 100 000 100 000

|

The remaining useful life of the plant contributed by Merlot Ltd is five years. The joint venture agreement stated that a manager will be appointed with the responsibility for growing, harvesting and marketing the grapes. The manager is also responsible for ensuring all plant of the joint venture is maintained to a satisfactory service level.

Additional information:

- a) During the year ended 30 June 2014 each of the investors made an additional cash contribution of $50 000 in exchange for an additional equal voting equity interest in Vineyards Pty Ltd.

- b) The harvest amounted to 300 tonnes of grapes, which the manager sold for $1 200 per tonne.

- c) Vineyards Pty Ltd. has adopted an accounting policy whereby plant is depreciated on a straight-line basis over its useful life. Accordingly the plant will be depreciated over five years.

The following financial statements were prepared for Vineyards Pty Ltd. For the year ended 30 June 2014.

| Balance sheet as at 30 June 2014 | |

| Assets:

Cash and cash equivalents Property, plant and equipment Sundry assets/account receivable Total assets

Liabilities: Trade and other payables Current tax payable Total liabilities Net assets

Equity: Share capital Retained earnings Total equity |

$

80 000 200 000 100 000 380 000

5 000 25 000 30 000 350 000

300 000 50 000 350 000 |

| Income statement for the year ended 30 June 2014 | |

|

Sales revenue Less Expense Profit from continuing activities before tax Less Income tax expense Profit for the year |

$

360 000 285 000 75 000 25 000 50 000 |

Required:

- i) Prepare the journal entries on 1 July 2013 in the books of Merlot Ltd and Malbec Ltd to record their investment in the jointly controlled entity – Vineyards Pty Ltd.

- ii) Prepare the adjusting journal entries required under equity method of accounting for the year ended 30 June 2014 in the financial statements of Merlot Ltd and Malbec Ltd in relation to their investment in the jointly controlled entity – Vineyards Pty Ltd.

iii) Explain how the journal entries required under (i) & (ii) could change if the joint venture agreement stated that due to the technical nature of the plant contributed by Merlot Ltd, it will be responsible for ensuring the plant is maintained to a satisfactory service level.

Question 3: (18 marks)

The following segment information is for Elegant Limited for the year ended 31 March 2010.

| Operating Segment | Segment Revenue

$ |

Segment Results (Profits/

(Losses) $ |

Segment Total Assets

$ |

Segment TotalLiabilities

$ |

| Manufacturing | 159,500 | 35,000 | 350,000 | 200,000 |

| Retail | 10,500 | (1,000) | 51,000 | 60,000 |

| Entertainment | 25,000 | (2,000) | 50,000 | 50,000 |

| Media | 25,000 | (1,500) | 50,000 | 28,000 |

| Chemicals | 35,000 | 21,000 | 120,000 | 100,000 |

| Travel | 12,000 | (5,000) | 100,000 | 150,000 |

| Publishing | 10,000 | 1,500 | 50,000 | 80,000 |

| Agriculture | 25,000 | 4,000 | 62,000 | 20,000 |

| General corporate | – | – | 75,000 | 200,000 |

| Total | 302,000 | 52,000 | 908,000 | 888,000 |

Required:

Prepare the segment disclosure for Elegant Limited for the year ended 31 March 2010 in accordance of AASB 8.

Question 4: (25 marks)

Report Writing on ‘Voluntary Disclosures in Australian Corporate Sector’ (Word length: maximum 1 200 words and at least 3 references).

Select two Australian companies from the list below in the same industry, which are listed on the Australian Stock Exchange (ASX) and having voluntary disclosures made on:

- a) ‘corporate governance’ and

- b) ‘corporate social responsibility’ (i.e. CSR or sustainability reporting of environmental, social and economic reporting or triple bottom line).

Find the most recent year-ending 2016-17 ‘annual report’ and ‘CSR report’ for each company applying ‘GRI guidelines’ (G4) (use company website or Global Reporting Initiative (GRI) web-site for the list of Australian companies providing sustainability report (https://www.globalreporting.org)).

- Qantas

- Virgin Australia

- Origin

- Santos

- OceanaGold

- BHP Billiton

In your essay, critically analysis and evaluate both ‘corporate governance’ ‘corporate and social responsibility’ reporting followed by each company and whether consistent with ensuring accountability and transparency to the satisfaction of shareholders/stakeholders. Identify the strengths and weaknesses of their reporting and disclosure as well as major differences along with your recommendations to advise how to minimise voluntary reporting and disclosure gaps between them.

Do not attach a copy of the corporate governance and sustainability reporting. Instead, to verify provide the web address of both companies.

Specific and descriptive criteria to follow:

(1) There must be an introduction and conclusion section and references, and website address of the selected companies where from corporate governance and sustainability reports are downloaded.

(2) There must be a very brief outline of the selected listed companies and their operating activities in the respective industry sector.

(3) A better understanding of the concepts of voluntary disclosure as well as reporting on corporate governance and CSR is expected.

(4) There must be an analysis of reporting practices of the companies whether ASX corporate governance and GRI disclosure guidelines (G4) are properly followed or not. The reporting practices of both companies must be compared and suggesting how more compliance is achievable. The strengths and weaknesses of reporting should be taken into account from the shareholders/stakeholders’ perspective as well as any relevant comments or recommendations therein.

Answer preview:

Words: 1,500