-

Аdvаnсеd Finаnсiаl Ассоunting

- Order Summary

- Type of assignment:Assessment

- Academic level:College Level

- Referencing style:APA

- Number of sources:1

- Subject:Accounting

- Client country:Australia (UK English)Assignment extract:

The topic of assignment on the last docx.

Please use my provide the accounts name and Number(chart of accounts).

These PPTs will help you to finish this assignment.

My first language is Chinese.

Assessment Instructions

Question 1: (22 marks)

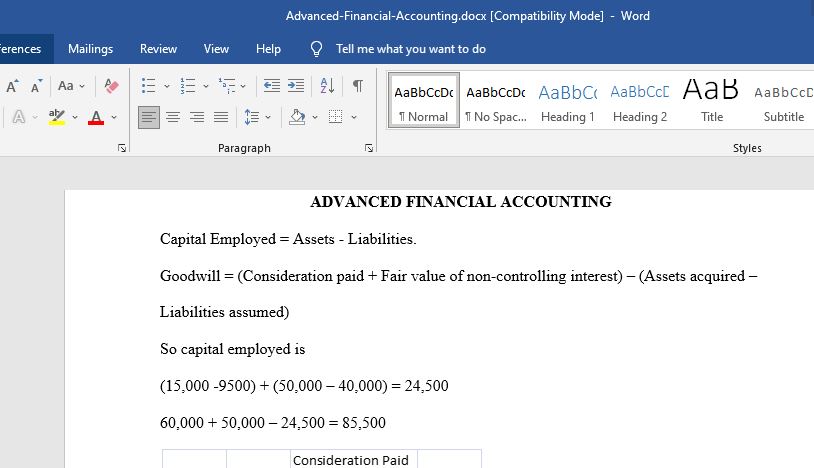

On 1 July 2008 S Ltd acquires 25% of the issued capital to C Ltd for a cash consideration of $60 000. At the date of acquisition, the shareholders’ equity of C Ltd is:

| Share capital

Retained earnings Total shareholders’ equity |

$75 000

$50 000 $125 000 |

Additional Information:

(a) On the date of acquisition, buildings have a carrying value in the accounts of C Ltd. of $40 000 and a market value of $50 000. The buildings have an estimated useful life of 10 years after 1 July 2008.

(b) For the year ending 30 June 2009 C Ltd. records an after tax profit of $15 000, from which it pays a dividend of $5 000.

(c) For the year ending 30 June 2010 C Ltd records an after tax profit of $50 000, from which it pays a dividend of $25 000.

(d) The tax rate is 30%.

Required:

Applying the equity method of accounting, calculate the amount of goodwill at the date of acquisition and prepare the journal entries for the year ended 30 June 2009 and 30 June 2010 as required by AASB 128.

Question 2: (35 marks)

On 1 July 2013, Merlot Ltd and Malbec Ltd entered into a joint venture by investing in a jointly controlled incorporated entity – Vineyards Pty Ltd. The purpose of the joint venture was to lease a 40-hectare vineyard for a five-year period at an annual lease rental of $200 000. Neither investor was a parent entity. Merlot Ltd and Malbec Ltd contributed the following assets to the joint venture in exchange for a 50% voting equity interest in Vineyards Pty Ltd.

| Carrying value $ Fair value $ |

| Merlot Ltd – Plant —————— 80 000 100 000

Malbec Ltd – Cash —————— 100 000 100 000

|

The remaining useful life of the plant contributed by Merlot Ltd is five years. The joint venture agreement stated that a manager will be appointed with the responsibility for growing, harvesting and marketing the grapes. The manager is also responsible for ensuring all plant of the joint venture is maintained to a satisfactory service level.

Additional information:

- a) During the year ended 30 June 2014 each of the investors made an additional cash contribution of $50 000 in exchange for an additional equal voting equity interest in Vineyards Pty Ltd.

- b) The harvest amounted to 300 tonnes of grapes, which the manager sold for $1 200 per tonne.

- c) Vineyards Pty Ltd. has adopted an accounting policy whereby plant is depreciated on a straight-line basis over its useful life. Accordingly the plant will be depreciated over five years.

The following financial statements were prepared for Vineyards Pty Ltd. For the year ended 30 June 2014.

Answer preview:

Word: 1,500